Dane County Spring ‘26: Still a Seller’s Market — Just Not the Same One

In our Fall 2025 Dane County Real Estate market update, we said to watch for inventory creeping up and days on market settling in at higher levels than the pandemic-era lows. Heading into Spring 2026, days on market are tracking in line with 2024-2025 while inventory is showing a meaningful year-over-year improvement.

Let’s dive into how this will impact buyers and sellers this spring.

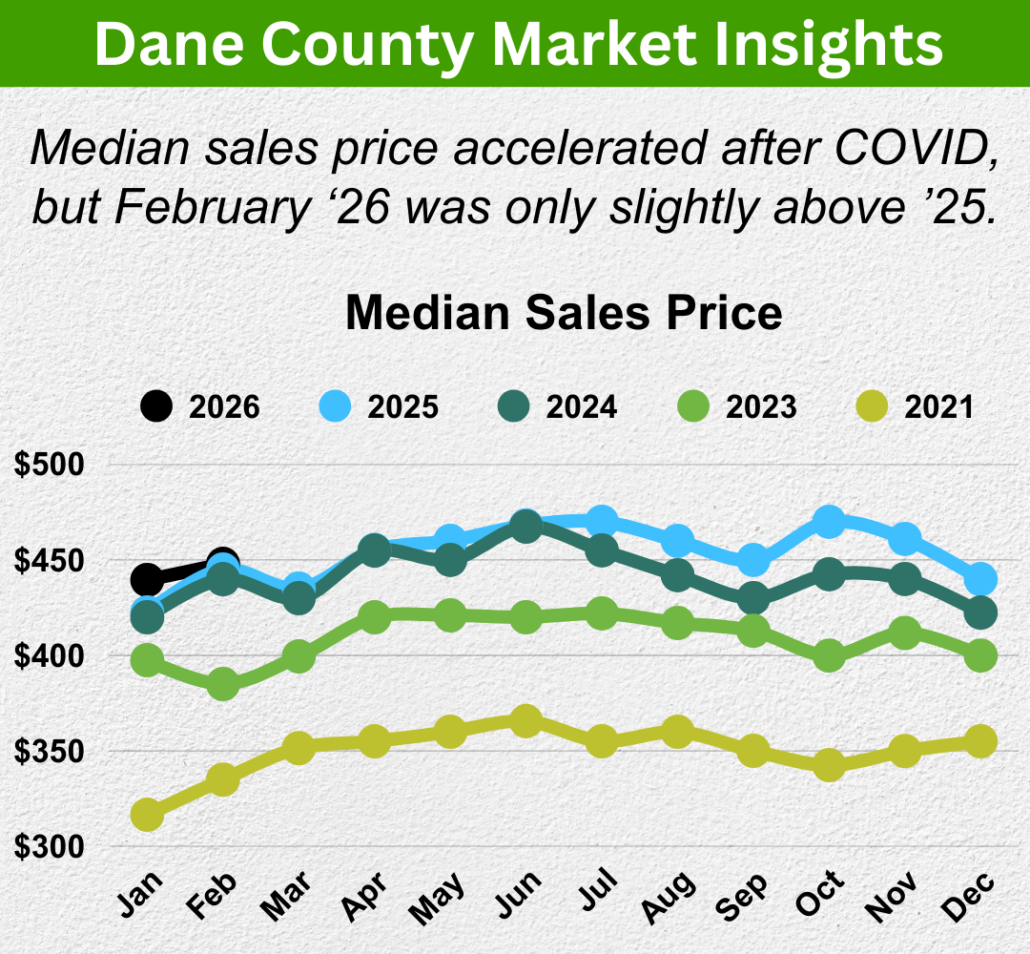

PRICES: A DURABLE FLOOR

February 2026 median sales prices are tracking slightly above February 2025, continuing a pattern of modest, steady appreciation rather than the sharp annual jumps of 2021–2023. Prices haven’t broken down — and they’re unlikely to — because the two things that cause real price declines (a demand collapse or a supply surge) simply aren’t present in Dane County. UW-Madison, Epic Systems, and the state government aren’t going anywhere, and neither is the demand they generate.

What’s worth watching is the price reduction count, which is up 35% over last year. That’s not a crash signal — in absolute terms, the numbers are still very low — but it is a pricing discipline signal. Overpriced homes are sitting. Well-priced homes are still moving. The seller’s advantage is intact, but it now requires a strategy rather than just showing up.

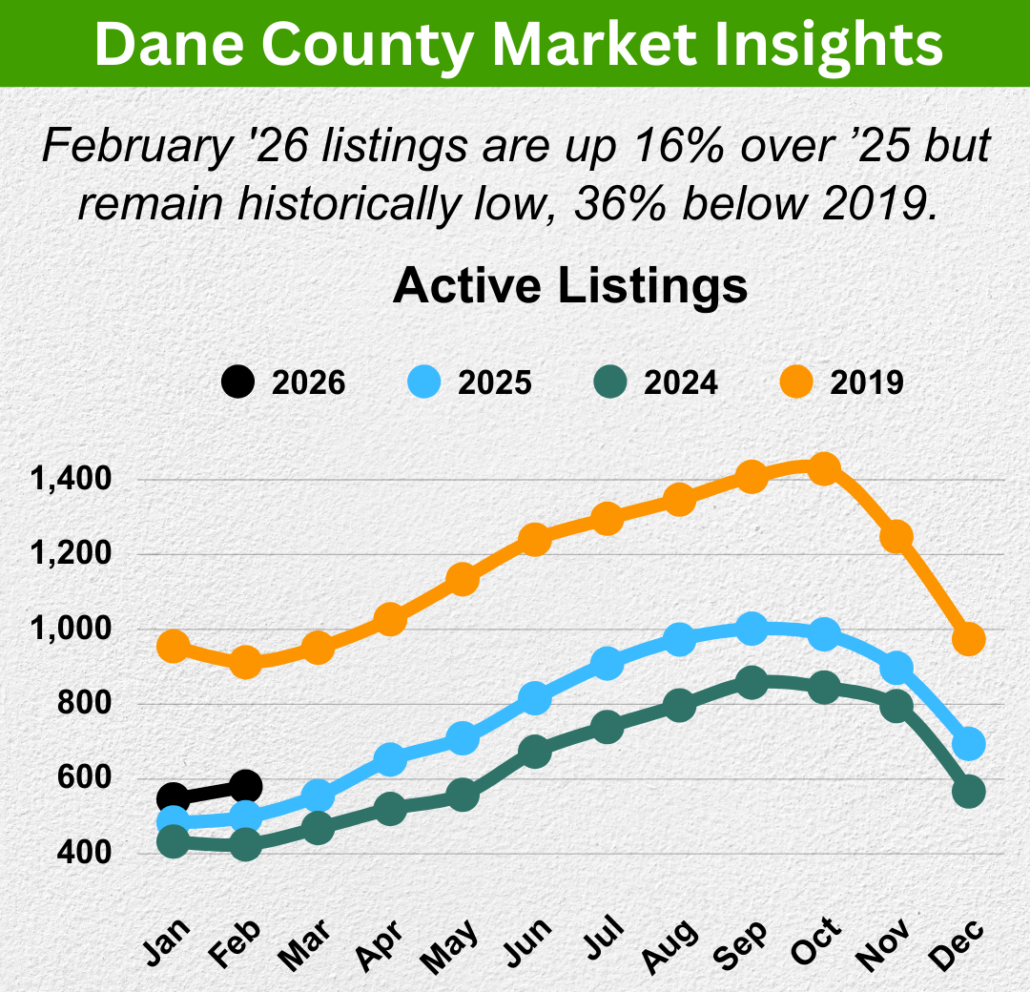

INVENTORY: BETTER, BUT NOT NORMAL

February 2026 active listings are up 16% over February 2025. That’s genuine progress and welcome news for buyers. But zoom out to the 2019 baseline, and we’re still 36% below what a normal Dane County market looked like — roughly 580 active listings today versus nearly 950 in February 2019. We are not in a balanced market. We are in a slowly improving seller’s market.

For context: Austin, in Travis County, Texas — with a profile similar to Madison’s (state capital, flagship university, strong in-migration, tech-driven economy) — doubled its active listings during a recent building surge, limiting price increases to a modest ~35% above 2019 levels. Dane County, hemmed in by lakes, wetlands, and limited zoning reform, has seen prices increase ~65% from that same 2019 baseline.

More Dane County inventory is coming, but not fast enough to change the fundamental supply-demand equation in the near term.

INTEREST RATES: CONTEXT MATTERS

Mortgage rates ended February at 5.98% — the first time below 6% since September 2022 — before economic uncertainty pushed them back toward ~6.25% as of March 15. The rate environment is moving in the right direction overall, but is volatile week to week. The long-term trend from the 7.8% peak in late 2023 is clearly downward, and every meaningful dip brings buyers off the sidelines quickly in a market this supply-constrained. Building your buying or selling strategy in this environment is important, and that’s exactly why our market experience matters.

The deeper rate story for Dane County is the lock-in effect. A large number of local homeowners are sitting on 2.75–3.25% mortgages from 2020–2021 and have had little reason to sell into a higher-rate market. As rates continue drifting lower over time, that calculus changes. More sellers coming off the sidelines means more inventory, which is ultimately healthy for everyone.

SPRING 2026 IN SUMMARY

Dane County’s Spring 2026 market is best described as a seller’s market in a slow normalization: prices are firming, inventory is improving at the margins, and rate volatility is creating uncertainty that’s best navigated with a clear strategy.

Buyers who are ready have more options and slightly more negotiating room than they’ve had in years.

Sellers who price correctly and get full MLS exposure are still winning.

The McGrady Group is ready to help you build a plan that works in this market, not the market from two years ago. Reach out anytime — we’d love to talk through your situation.

Warm regards,

Matt & Seth

The McGrady Group